If you're worried about high commissions when selling your home, there might be a larger expense you haven't considered – capital gains. Did you know that you could potentially be facing as much as a 39% capital gains tax when you sell your home in California?

If you're thinking of selling your home in California, it's crucial to understand how capital gains work when you sell your primary residence.

Disclaimer: First and foremost, I want to clarify that I'm not a tax professional. The tax code can be complex and confusing, and its application varies from person to person. To get a clear understanding of your specific tax situation and capital gains, I strongly encourage you to consult with a tax professional. If you need recommendations for a reliable tax expert, feel free to call me, and I'll be happy to assist you. Ryan Nickell (408) 857-5153

Misconceptions about Capital Gains

They say that two things are certain in life: death and taxes. If you've accumulated substantial equity in your home, understanding capital gains is essential to anticipating the tax liability you might face when selling.

In my experience, many homeowners are taken aback by the amount of capital gains they owe upon selling their homes. There are numerous misconceptions about how capital gains work, especially when it comes to the sale of a primary residence. Much of the confusion can be traced back to changes in the tax code dating back to 1997, which allowed you to defer your capital gains if you purchased a property of higher value after selling.

However, the current tax code is notably different, only allowing exemptions for the first $500,000 in profits for married couples and $250,000 for single individuals. Anything beyond these exemptions is considered a capital gain.

Understanding How to Calculate Your Capital Gain

Let's work through an example to illustrate how to calculate your capital gains.

In our example, the homeowners purchased their home for $250,000 and are now selling it for $2 million.

The first step is to determine your basis. Your home's cost basis is usually what you initially paid for it. The basis can also be adjusted if your spouse passed away or if you acquired the property later in a divorce settlement.

For the sake of simplicity, let's assume the original purchase price is the basis in this example. So, in our example, the homeowners purchased their home for $250,000.

In addition to the basis, you can add any costs incurred to acquire the home, such as closing costs. Let's assume the homeowners had $5,000 in closing costs when they originally purchased their home.

Next, you can factor in the costs of improvements made to the home, like additions, remodeling, heating or cooling systems, new windows, and landscaping improvements. Essentially, anything that enhances your home's value can be considered an improvement. For our example, let's assume the homeowners spent a total of $100,000 on improvements.

Then, you should consider the costs incurred while selling your home, such as commissions and closing costs. In this example, let's assume these costs are approximately 5%, which would amount to $100,000 for a $2 million home.

Finally, you can apply your exemption, which is $500,000 for a couple selling their primary residence.

To calculate the capital gain, you deduct the basis, costs incurred during purchase, improvement costs, selling costs, and the exemption. In our example, the calculations come out to $955,000. The difference between the sale price and these deductions is the capital gain, which, in this example, is $1.045 million.

It's essential to note that the capital gain is distinct from your proceeds. The proceeds depend on any outstanding loans on the property and your selling costs.

Calculating Your Tax Liability

Now, let's get into the complex part – calculating your capital gains tax liability. This involves understanding your filing status and your total capital gains for the calendar year.

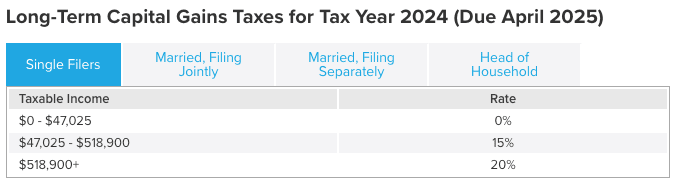

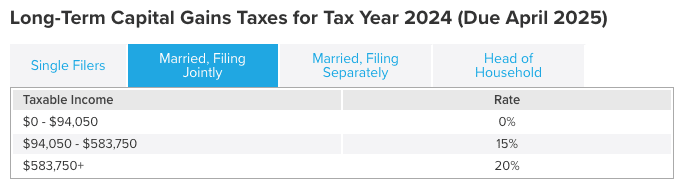

Both federal and California capital gains rates are based on a tiered schedule, where higher capital gains result in higher tax rates. For instance, married couples who file jointly have a zero federal capital gains rate on the first $80,000 in capital gains, which means no federal tax on the initial $80,000. However, any capital gains above $501,601 are taxed at a 20% rate.

Here are the 2024 capital gains rate tables for Federal Long Term Capital Gains.

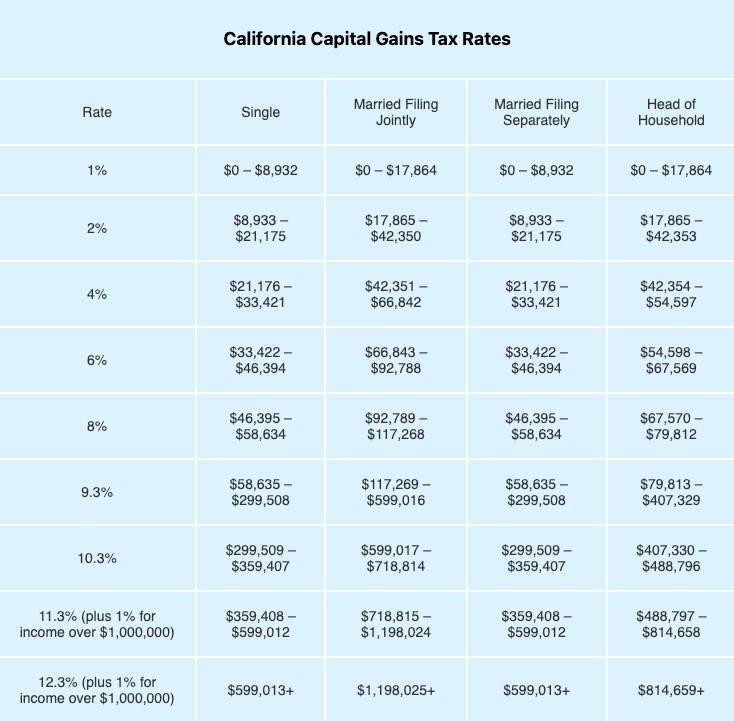

And here are the 2024 California Capital Gains Rate Table

Keep in mind that if you earn over $250,000 as a married couple or $200,000 as an individual, including your real estate sale gains, you are subject to an additional 3.8% tax.

As you can see, this can become quite complex. This video is intended to provide a general understanding and is not meant to determine your exact tax liability when you sell your home. For that, you should consult a tax professional, and I'm happy to recommend one if needed.

A Couple of Important Points

Regarding withholding taxes when you sell, the federal government doesn't require withholding if the home is your primary residence and you are not a foreign national. In other words, if you have a green card or are a citizen. However, California does require withholding if it is not your primary residence.

Lastly, keep in mind that our tax system is constantly evolving, with significant changes often occurring when new administrations take office. As of my last update, the Biden Administration had proposed raising capital gains tax rates for top earners, those making over $1 million or more, to 39.6%, essentially treating it as regular income. Please verify the current status of this proposal.

Conclusion

In recent decades, we've witnessed significant appreciation in local property values. While this is excellent for wealth creation, the tax consequences are often overlooked and poorly understood. The purpose of this article is to shed light on the costs associated with selling a property, helping you make informed financial decisions when selling your home.

I'm not qualified to provide tax advice, but I'm here to answer any general questions you may have and guide you in the right direction to obtain the information you need. If you'd like to schedule a free, no-obligation phone call or meeting, please don't hesitate to contact me directly, Ryan Nickell (408) 857-5153.