Exploring Tax Mitigation Strategies: Charitable Remainder Trusts and Charitable LLCs

When considering selling a highly appreciated asset, one of the most significant concerns is how to mitigate capital gains taxes effectively. Two innovative strategies that could help reduce or eliminate these taxes are the Charitable Remainder Trust (CRT) and the Charitable LLC. Whether these approaches—or others like a 1031 exchange—are worth pursuing depends on individual goals and circumstances. However, these tools can potentially save taxpayers hundreds of thousands of dollars while offering additional financial and philanthropic benefits.

Understanding the Charitable Remainder Trust (CRT)

The CRT has been a well-established tax mitigation tool since the 1960s. It is most useful for taxpayers facing a considerable taxable event, particularly those who do not need immediate access to all sale proceeds. The CRT works by transferring ownership of an appreciated asset (such as real estate, stocks, or art) into a trust before selling it. The proceeds of the sale are then reinvested, and the trust provides a fixed income to the donor (or donors) for life or a specified term of years.

Key Benefits of a CRT:

- Tax Savings: By donating the asset to the trust before selling, capital gains taxes are avoided.

- Fixed Income: Beneficiaries receive income for life or a set term.

- Charitable Deduction: A sizable deduction is available based on the charitable remainder's present value.

- Asset Protection: Assets in the trust are protected from creditors.

There are two main types of CRTs:

- Charitable Remainder Unitrust (CRUT): Pays a fixed percentage of the trust's value, which is recalculated annually. This provides an inflation hedge and allows additional assets to be added over time.

- Charitable Remainder Annuity Trust (CRAT): Pays a fixed dollar amount annually, but no additional contributions can be made after it is established.

For those interested in learning more, a detailed video on CRUTs is available here: CRUT Deep Dive with Mark Kohler.

Considerations for Using a CRT

A CRT may not be viable if the property being sold carries substantial debt since debt cannot be donated to a 501(c)(3). For homeowners with mortgages, paying off the debt before contributing the asset to the trust is necessary. However, for those who can navigate this hurdle, a CRT can be a powerful vehicle to maximize returns and minimize tax burdens.

Exploring the Charitable LLC

The Charitable LLC, also known as the "100-to-1 plan," offers another tax mitigation pathway. This strategy involves transferring an appreciated asset into a specialized LLC, which then donates the asset to charity. A unique aspect of this strategy is its ability to use life insurance policies as collateral for loans, providing liquidity without triggering taxable events.

Key Features of the Charitable LLC:

- Larger Charitable Deductions: Often greater than those associated with CRTs.

- Liquidity Through Loans: Funds can be accessed tax-free via loans against the LLC’s assets.

- Flexibility: Offers significant customization depending on financial and philanthropic goals.

Although less common than CRTs, the Charitable LLC is gaining popularity among high-net-worth individuals, including notable folks like Mark Zuckerberg.

Comparing CRTs and Charitable LLCs

| Feature | CRT | Charitable LLC |

|---|---|---|

| Charitable Deduction | Moderate | Larger |

| Upfront Costs | Lower | Higher |

| Withdrawal Tax Treatment | Favorable (income tax) | Tax-free via loans |

| Track Record | Established since 1960s | Newer but tested |

Next Steps

For those interested in these strategies, consulting with experienced tax strategists and trust attorneys is essential. Professionals like Mark Kohler, who specializes in CRTs, and Bruce Jones, known for his expertise with Charitable LLCs (handbook here), can provide detailed insights and implementation support. Both approaches require some lead time, so early planning is critical. Here is Bruce Jone's contact phone number 800-997-7646 or even better fill out his contact form on his website: www.taxwealth.com

Here’s the link to Mark’s YouTube page and the link to Mark’s firm for getting started on the CRUT.

And last, here is the modeling template PDF and the CRT handbook for your reference as well.

Our Commitment

At our firm, we aim to maximize the returns on every property sale. By providing access to strategies like CRTs and Charitable LLCs, we help clients make informed decisions that align with their financial goals. For further information, we have included attachments, such as modeling examples and educational handbooks, to deepen your understanding of these approaches.

If you have any questions or wish to explore these options further, we encourage you to reach out. We are happy to connect you with the right professionals and assist in any way necessary.

A little more about us

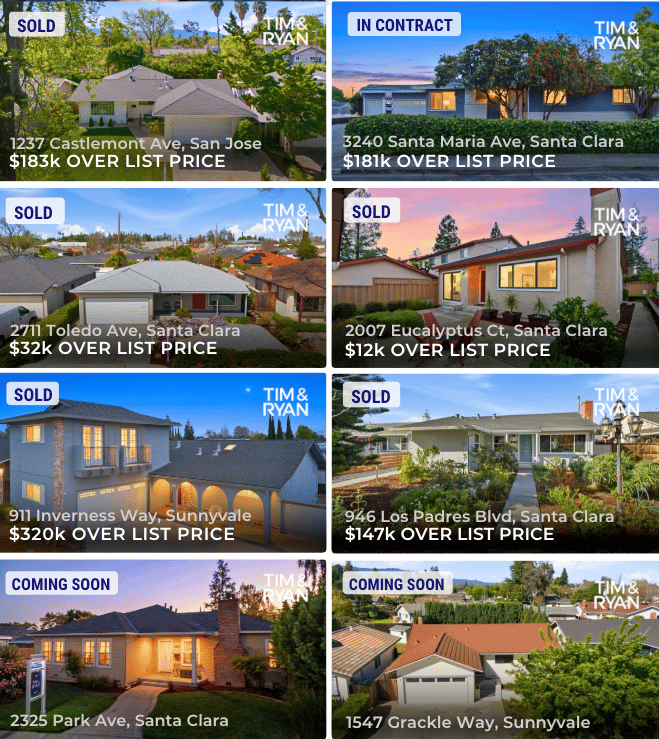

Here is a selection of our most recent sales, which offer a few insights into our marketing approach and the style of strategic remodels/improvements we coordinate and oversee to maximize ROI relative to cost and time. We're happy to run point and project manage any improvements you sign off on. We do dozens of remodels a year, so we deal with the City and various contractors and subs repeatedly. Our main goal in every situation is to do what makes sense (in cost and time) to maximize your return. If we can put X in and get 2-3X out without taking a great deal of time, then we'll always recommend that.

Additionally, here’s an episode of American Dream TV that we were featured on a few years back before we set out on our own and our Zillow profile, which captures our most recent transactions and 100+ reviews, something we take great pride in. (Unlike larger real estate “Teams” or “Groups,” where their Zillow metrics absorb everyone’s on the team, these transactions and reviews are from clients of only the two of us and no one else, as it would be us and no one else overseeing any repairs and improvements and representing the property in-person during any open houses.)

Additionally, Deborah got $719,000 over the as-is appraisal value and Zestimate, while Holly (the Cupertino seller who utilized a CRUT to eliminate her capital gains) and the Cook family were kind enough to record video testimonials of their experiences working with us. We have other reviews and testimonials we're happy to share, if need be.

How to sell for more video below

In closing, we prefer to keep conversations like ours to more freeform and focused on your questions, vice walking you through a standardized one-size-fits-all presentation. The downside of that is there’s often areas that may be of interest to you that we never touch upon. Accordingly, it’s likely some of these topics — or new questions — will come to mind in the weeks ahead and after some additional reading. If so — if you have any questions or wish to further discuss the CRT, Charitable LLC, or anything else with us, please don’t hesitate to call, text, or email at any time. Thanks again for your time reading this and we look forward to continuing the conversation.

Happy to help,